- Call for a Free Consultation, Near You.

- Call for a Free Consultation, Near You.

- SUFFOLK

(631)-271-3737 , QUEENS (718)-751-0226

(631)-271-3737 , QUEENS (718)-751-0226 - NASSAU (516)-307-0262 , BROOKLYN (347)-508-9316

- Exceptional Legal Representation Throughout

- Long Island and New York, Since 1993.

- SUFFOLK (631)-271-3737 , QUEENS (718)-751-0226

- NASSAU (516)-307-0262 , BROOKLYN (347)-508-9316

- Exceptional Legal Representation Throughout Long Island and New York, Since 1993.

(631)-271-3737

(631)-271-3737 (718)-751-0226

(718)-751-0226 (516)-307-0262

(516)-307-0262 (347)-508-9316

(347)-508-9316

QUEENS LOCATION

QUEENS LOCATION

118-35 Queens Blvd Tower,

Suite 400

Queens, NY 11375

(718)-751-0226

By Appointment Only

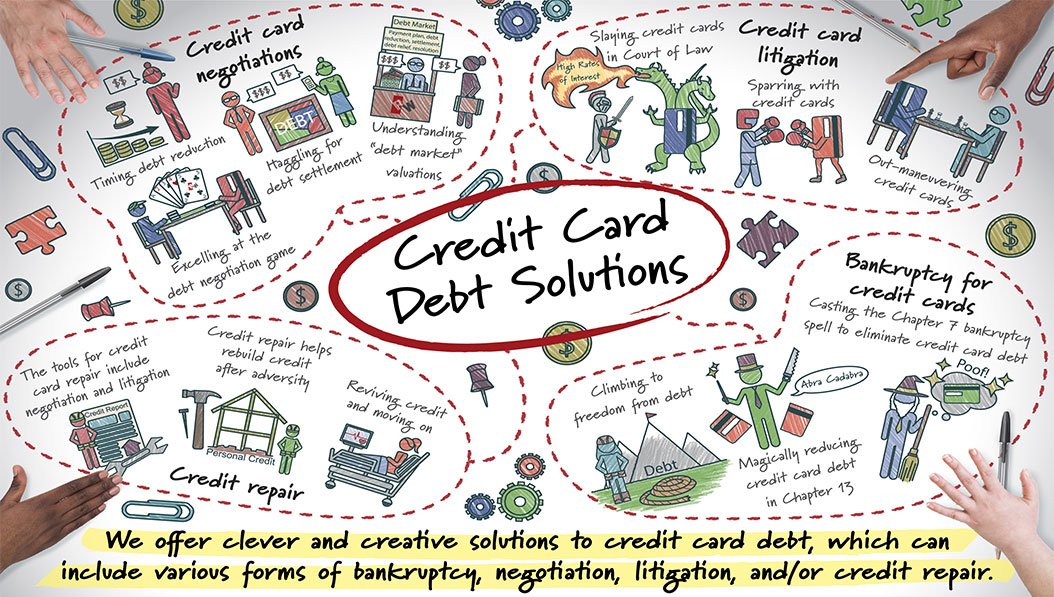

Credit Card Solutions

Credit Card Debt Relief – Nassau & Suffolk Counties, Long Island

Mounting credit card debt is usually the first sign of financial hardship, and the resolution of such debt is often key to avoiding further financial problems.

- Negotiated Settlement of Credit Card Debt

- Bankruptcy Relief of Credit Card Debt

- Litigation Defense of Credit Card Debt

- How Our Law Office Can Help You With Credit Card Relief

Credit cards and other personal unsecured loans are the most prevalent debt for consumer debtors. There are several way to legally deal with credit card debts as follows: a) Negotiated Settlements, b) Bankruptcy, and/or c) Litigation. The Law Office of Ronald D. Weiss, P.C. represents clients in all manner of credit card debt relief. We can through extensive negotiations reach settlement agreements with all or most of your creditors, or use bankruptcy laws to eliminate your credit card bill, or in appropriate situations challenge the credit card obligations by litigating them in court.

Credit cards and other personal unsecured loans are the most prevalent debt for consumer debtors. There are several way to legally deal with credit card debts as follows: a) Negotiated Settlements, b) Bankruptcy, and/or c) Litigation. The Law Office of Ronald D. Weiss, P.C. represents clients in all manner of credit card debt relief. We can through extensive negotiations reach settlement agreements with all or most of your creditors, or use bankruptcy laws to eliminate your credit card bill, or in appropriate situations challenge the credit card obligations by litigating them in court.

Negotiated Settlement of Credit Card Debt

Credit cards can be aggressively settled, especially when the credit card companies are aware that the alternative may be a bankruptcy case to completely eliminate the credit card debt.

Credit cards can be aggressively settled, especially when the credit card companies are aware that the alternative may be a bankruptcy case to completely eliminate the credit card debt.

i) The Need for Credit Card Negotiations – Most of the clients coming to our office with credit card debt are interested in bankruptcy solutions since they are usually more thorough and certain than negotiated settlements. However, there are many instances where our clients have either too much in terms of assets or income to file a bankruptcy case that would sufficiently alleviate their debt situation. In other situations the debt is not sufficiently overwhelming to require a bankruptcy case and the client may be better served by negotiating a lower payment for debt that they can pay.

ii) How Our Office Can Help You Negotiate a Settlement with Your Credit Cards – In situations where bankruptcy is not possible or desired by a client, our office can negotiate “lump sum” settlements for payment plans with the client’s creditors. Given that we are a bankruptcy firm and routinely file bankruptcy cases creditors are informed that we are exploring bankruptcy options but would prefer a negotiated solution. Often we are able to obtain a lump sum resolution which reduces the debt to 33-50% of the debt. If the client needs to negotiate a payment plan, the loan will not usually be so drastically reduced but it will be reduced in terms of interest and monthly payments.

iii) Our Method of Negotiating with Credit Cards– Because clients often come to use with several or numerous credit cards that require negotiation, we prepare an Excel sheet that lists all the creditors and their pertinent contact and loan information. Then we systematically write and call all the cards in pursuit of negotiated settlements. Using this method we can best track the progress with our settlement efforts and advise our clients as to our progress.

Credit card negotiations can be involved and experience and the leverage of other legal options, are all helpful. The Law Office of Ronald D. Weiss, P.C. regularly represents its Long Island and New York clients in credit card negotiations.

Bankruptcy Relief of Credit Card Debt

A Chapter 7 bankruptcy case will eliminate most or all of a client’s debt and will allow the client to obtain a fresh financial start.

A Chapter 7 bankruptcy case will eliminate most or all of a client’s debt and will allow the client to obtain a fresh financial start.

A Chapter 7 bankruptcy case will eliminate most or all of a client’s debt, and will allow the client to obtain a fresh financial start. A Chapter 7 case is a highly effective tool in dealing with burdensome credit card and other unsecured debts, such as medical bills and personal loans. A Chapter 7 case is especially helpful when the client cannot pay their present bills and faces the prospect of creditor harassment, collection actions and bad credit.

i) Initiating a Chapter 7 Case and the “Automatic Stay” – The Chapter 7 case starts when legal documents, called a bankruptcy petition, schedules and statement of financial affairs, are filed with the bankruptcy court; these documents which are intended to disclose all of the client’s financial affairs at the time of the filing, contain information about all of the client’s assets, liabilities, income and expenses at the time the case is filed. Such information is obtained by our firm’s meeting with the client and doing an “intake” where we ask many questions about the client’s finances and collect documentation for the file, including proof of income, tax returns, bank statements, and the client’s bills and invoices. We also run a credit report, and where requested a judgment lien search, so that we can properly list a client’s creditors and debts on their bankruptcy schedules. Prior to filing the bankruptcy case the client must complete a pre-filing session of “credit counseling” which is a session, by phone or by internet, with a credit counsellor who analyzes the clients finances in a private session with the client. Upon the filing of the Chapter 7 case, the client will be immediately protected from their creditors with an “automatic stay” which causes creditors to immediately stop all collection activity and to release bank restraints and wage garnishments.

ii) Issue of Potential “Equity” in Assets – During the Chapter 7 case the client will need to attend a creditors’ meeting where the client is interviewed by a Chapter 7 trustee whose role is to determine whether there are potential assets with equity that may be sold to satisfy the claims of creditors. Most Chapter 7 cases are considered to be “no asset” cases in that there are no assets available to satisfy the claims of creditors. The reality is that most Chapter 7 debtors do have assets, but their cases nonetheless are considered to be “no asset” cases because their assets are not considered to have significant equity. What diminishes from the potential “equity” in particular assets are liens, such as mortgages and car loans, and statutory exemptions which protect a certain amount of equity. Exemptions are amounts in value in particular assets that under the law that are unavailable to creditors. In New York State we are currently able to select from either the exemption scheme offered under New York State law or the exemption scheme offered by federal law. The New York State exemption scheme is generous in it’s “homestead exemption” or in protecting a client’s residence for the amount of $150,000. per person owning and actually living in the home. The federal exemption scheme, which is different, is more generous with better protection for personal property in that it gives a “wildcard” exemption of approximately $12,500. per debtor which can be used towards protecting any item of personal property, including tax refunds, bank accounts and vehicles. Most clients keep all of their property including their vehicles, homes and personal possessions as long as they stay current with the payments on these items and do not have too much equity in such property.

iii) Issue of “Avoidable Transfers” – Closely related to the issue of potential equity in assets, is the issue of “avoidable transfers”. These can be “preferences”, or payments to creditors made 90 days prior to the bankruptcy case for third party creditors, or one year prior to the bankruptcy filing for “insiders” (or relatives or close associates of the debtor). These can also be “fraudulent transfers” or transfers for less than reasonable value six years prior to a bankruptcy case, usually made to relatives or close associates of the debtor. Avoidable transfers are not alway obvious and what sometimes can appear to be an innocent transaction, under bankruptcy law can potentially be alleged to be an avoidable transfer.

iv) Issue of Income Level – In addition to the issues of assets and transfers, there is the issue of income level, in that persons qualifying for Chapter 7 relief can not have income above a certain level based on their household size. The client needs to have an average of six (6) months gross income that is below a certain median level in New York State, or alternatively pass a means test which takes into account the client’s necessary expenses in determining if the client qualifies for Chapter 7 relief (despite their income being above the median level). The income issue needs to be carefully analyzed prior to filing a Chapter 7 case by comparing the client’s household income, relative to their family size, and their necessary allowed expenses, in determining whether the client should be able to file for Chapter 7 relief. Because the average household income on Long Island is higher than in many other parts of New York State, it is important to carefully average the client’s household gross household income for the 6 months prior to the filing of the bankruptcy petition. In many cases that are close to the line, this can be a tricky assessment, since even if the household income exceeds the median income level, there are many allowances for various essential spending that could potentially allow a “close” case under the proper circumstances to file despite income that is over the median. Where the gross household income does not pass the means test, the client can still proceed to obtain relief under Chapter 13, which does not have the same filing limits as Chapter 7.

v) Issue of “Abusive” Debt – Finally, there is also the potential issue of the abusive incurring of debt prior to filing a bankruptcy case. The incurring of a large amount of cash advances and balance transfers shortly prior to filing a bankruptcycase, may be monitored by creditors who may object to the discharge of such debt. In some cases where the client has incurred such recent “cash” debt, a certain amount of payments and waiting are advisable prior to filing the bankruptcy case.

vi) Avoiding Judicial Liens Against the Client’s Home – While the Chapter 7 case can eliminate unsecured debt against the debtor himself, it cannot do the same for secured liens filed against the debtor’s property. To the extent that prior to the bankruptcy filing, a creditor had obtained a judgment and had liened it against the client’s home, the client can move to avoid the judicial lien, based on it’s interfering with the client’s exercise of his homestead exemption. If there is no equity in the client’s home other than equity protected by the homestead exemption, such a motion can successfully avoid the judicial liens.

vii) Concluding a Bankruptcy Case and the Bankruptcy “Discharge” – The goal in each Chapter 7 case is to obtain a “discharge” order, or legal forgiveness for the debt, so that the client can obtain a “fresh start” and be able to rebuild their credit. The discharge of the debt makes permanent what the automatic stay protected against temporarily. Essentially, most of the client’s unsecured debts are now legally forgiven. There are some exceptions to the discharge, they are most student loans, most taxes and most child or matrimonial support obligations. Most clients discharge all their unsecured debt, although clients are able to voluntarily keep or “reaffirm” certain debts.

viii) The Potential Benefits of Chapter 7 and the Role of Our Law Office – Chapter 7 is the most frequently used type of bankruptcy case and is often used by individuals who are overwhelmed by debts – including credit card debt, medical bills, repossession/foreclosure deficiencies or other debt – to eliminate their legal obligation to pay (or to “discharge”) such debt. Most Chapter 7 cases take approximately four (4) months and are highly effective in allowing a client to quickly deal with and resolve their problems by eliminating their obligation to pay debt that is beyond their ability to pay. However, a bankruptcy attorney needs to carefully review a client’s circumstances with the client to determine that the client does not have issues that may complicate the case, like major assets with significant equity; income that may be too high; alleged “avoidable transfers”; and/or debt taken by the client that may be deemed to be abusive and/or in bad faith.

Chapter 7 cases, like other types of bankruptcy cases can effectively help a client deal with its debt, including overwhelming credit card debt, however, a Chapter 7 case be complex, and to effectively proceed in a Chapter 7 case an individual should be represented by a bankruptcy attorney. The Law Office of Ronald D. Weiss, P.C. can discuss and advise you about Chapter 7 bankruptcy and how and whether it can help give you relief for your overwhelming credit card debt.

The Law Office of Ronald D. Weiss, P.C. regularly represents Long Island and New York clients seeking to discharge excessive credit card debt in Chapter 7 cases before the United States Bankruptcy Court and can review with you issues relevant to a potential Chapter 7 case.

Litigation Defense of Credit Card Debt

Litigation Defense allows a defendant to use procedure and the legal process of the court system to challenge alleged credit card debt and to assert their legal rights.

Litigation Defense allows a defendant to use procedure and the legal process of the court system to challenge alleged credit card debt and to assert their legal rights.

Many of the clients of The Law Office of Ronald D. Weiss, P.C. are faced with potential litigation or collection actions by their creditors. Usually the majority of such creditors are owed money for credit cards. One response to litigation by a creditor, especially one for significant amounts, which are disputed, is to defend against such litigation. Our firm can help the client answer the summons and complaint that initiate the litigation. This needs to be done within 20-30 days after service of the summons and complaint. Such answer is one out of several documents that are usually filed as part of a litigation defense. Other documents may include a motion to dismiss, if applicable, and a response to a motion for summary judgment. Defending the litigation proceeding allows the client to assert any defenses they may have to the manner in which such litigation was initiated. A litigation defense also gives the client and our firm notice as to the status of the litigation and prolongs the proceeding. In some instances a client may have a strong defense, which may cause a litigation to be dismissed. Defenses asserted by our office look at issues such as defective service, the existence and applicability of the alleged loan documents, the clarity of the alleged loan terms, the appropriateness of the loan amount, the amount of interest and fees charged by the credit card. Often our office would engage in discovery demands to try to obtain documents and/or information regarding the alleged debt and to help with potential defenses.

Defending the collection actions by credit cards allows the client to assert any defenses they may have as to the manner in which such collection action was initiated and/or the manner such credit card debt was extended.

The Law Office of Ronald D. Weiss, P.C. regularly defends its clients in court and litigation defense is one of the strategies used to challenge alleged credit card debt obligations, and/or to win time and leverage for our clients to negotiate with their credit cards.

How Our Law Office Can Help You With Credit Card Relief

The experience of the attorney representing the client is a critical factor in the client’s success when attempting to obtain relief from credit card and other unsecured debts. Since 1993 we have successfully represented thousands of clients residing in Long Island, Nassau County & Suffok County finding relief for their credit card and other unsecured debt. We have helped many of them permanently eliminate unsecured debt and re-establish their financial stability. When an individual owes unsecured debt, all of their legal options need to be carefully pursued: a) Negotiated Settlements, b) Bankruptcy, and/or c) Litigation Defense. Let us help you in your efforts to save your home with experience and expertise that is both affordable and personable.

The experience of the attorney representing the client is a critical factor in the client’s success when attempting to obtain relief from credit card and other unsecured debts. Since 1993 we have successfully represented thousands of clients residing in Long Island, Nassau County & Suffok County finding relief for their credit card and other unsecured debt. We have helped many of them permanently eliminate unsecured debt and re-establish their financial stability. When an individual owes unsecured debt, all of their legal options need to be carefully pursued: a) Negotiated Settlements, b) Bankruptcy, and/or c) Litigation Defense. Let us help you in your efforts to save your home with experience and expertise that is both affordable and personable.

Our consultations are free, the advice may be invaluable.

Please call us at (631) 271-3737, or e-mail us at weiss@ny-bankruptcy.com for a free consultation to discuss credit card relief options in greater detail.

Contact Us

- HOURS OF OPERATION

- Monday – Friday – 8:30 AM – 8:30 PM

- Saturday – Sunday – 10 AM – 6 PM

Contact Us

Tell Us About Your Situation