- Call for a Free Consultation, Near You.

- Call for a Free Consultation, Near You.

- SUFFOLK

(631)-271-3737 , QUEENS (718)-751-0226

(631)-271-3737 , QUEENS (718)-751-0226 - NASSAU (516)-307-0262 , BROOKLYN (347)-508-9316

- Exceptional Legal Representation Throughout

- Long Island and New York, Since 1993.

- SUFFOLK (631)-271-3737 , QUEENS (718)-751-0226

- NASSAU (516)-307-0262 , BROOKLYN (347)-508-9316

- Exceptional Legal Representation Throughout Long Island and New York, Since 1993.

(631)-271-3737

(631)-271-3737 (718)-751-0226

(718)-751-0226 (516)-307-0262

(516)-307-0262 (347)-508-9316

(347)-508-9316

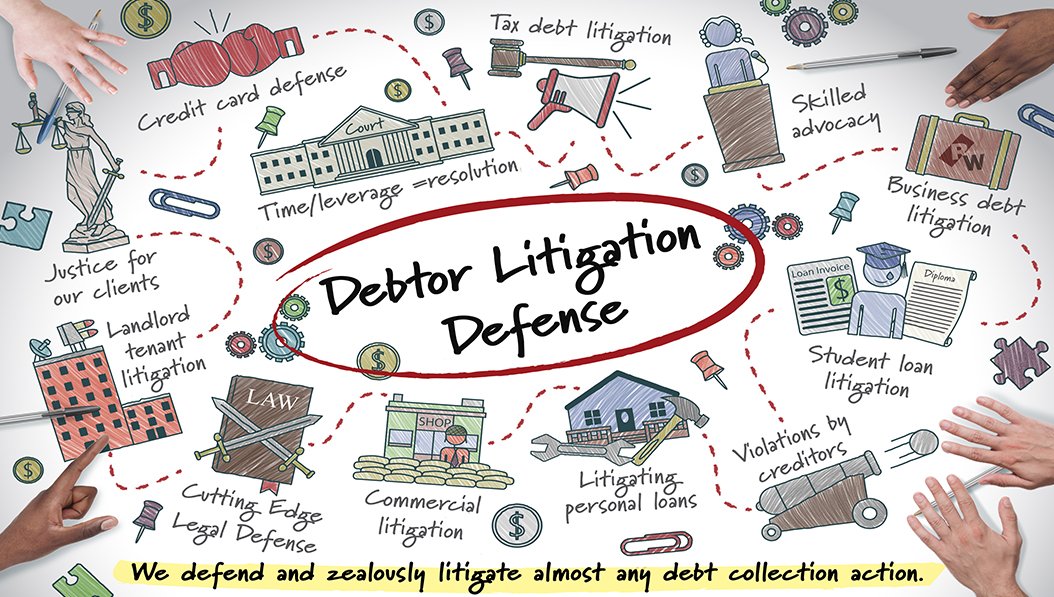

Debtor Litigation Defense

Debt Collection Defense Lawyer For Law Suits Commenced by Creditors – Nassau & Suffolk Counties, Long Island

Defending Debt Collection in Court – Debtor Litigation Defense allows a defendant to use procedure and the legal process of the court system to challenge alleged debt and to assert their legal rights.

- LITIGATION DEFENSE

- LITIGATION – ADDITIONAL TEXT OUTLINE

- KINDS OF LITIGATION –

- Business Debt Litigation

- Student Loan Debt Litigation

- Credit Card Debt Litigation

- Tax Debt Litigation

- Landlord-Tenant Litigation

- Foreclosure Defense Litigation

- Medical Debt Defense Litigation

- Credit Repair Litigation and Other Consumer Rights Litigation

- HOW WE CAN HELP WITH LITIGATION AND HOW TO GET STARTED –

- WHY USE OUR OFFICE FOR LITIGATION

Many of the clients of The Law Office of Ronald D. Weiss, P.C. are owe alleged debt that they are unable to pay or dispute the liability and/or amount of the alleged debt and are faced with potential litigation or collection actions by their creditors. One response to litigation by a creditor, especially one for significant amounts, which are disputed, is to defend against such litigation. Our firm can help the client answer the summons and complaint that initiate the litigation. This needs to be done within 20-30 days after service of the summons and complaint. Such answer is one out of several documents that are usually filed as part of a litigation defense. Other documents may include a motion to dismiss, if applicable, and a response to a motion for summary judgment. Defending the litigation proceeding allows the client to assert any defenses they may have to the manner in which such litigation was initiated. A litigation defense also gives the client and our firm notice as to the status of the litigation and prolongs the proceeding. In some instances a client may have a strong defense, which may cause a litigation to be dismissed. Defenses asserted by our office look at issues such as defective service, the existence and applicability of the alleged loan documents, the clarity of the alleged loan terms, the appropriateness of the loan amount, the amount of interest and fees charged by the credit card. Often our office would engage in discovery demands to try to obtain documents and/or information regarding the alleged debt and to help with potential defenses.

Many of the clients of The Law Office of Ronald D. Weiss, P.C. are owe alleged debt that they are unable to pay or dispute the liability and/or amount of the alleged debt and are faced with potential litigation or collection actions by their creditors. One response to litigation by a creditor, especially one for significant amounts, which are disputed, is to defend against such litigation. Our firm can help the client answer the summons and complaint that initiate the litigation. This needs to be done within 20-30 days after service of the summons and complaint. Such answer is one out of several documents that are usually filed as part of a litigation defense. Other documents may include a motion to dismiss, if applicable, and a response to a motion for summary judgment. Defending the litigation proceeding allows the client to assert any defenses they may have to the manner in which such litigation was initiated. A litigation defense also gives the client and our firm notice as to the status of the litigation and prolongs the proceeding. In some instances a client may have a strong defense, which may cause a litigation to be dismissed. Defenses asserted by our office look at issues such as defective service, the existence and applicability of the alleged loan documents, the clarity of the alleged loan terms, the appropriateness of the loan amount, the amount of interest and fees charged by the credit card. Often our office would engage in discovery demands to try to obtain documents and/or information regarding the alleged debt and to help with potential defenses.

Defending the collection action proceeding allows the client to assert any defenses they may have as to the manner in which such collection action was initiated and/or the manner such debt was extended.

Our clients are also often faced with foreclosure procedures against their homes. Foreclosure defense is a specific kind of litigation defense and more detailed information about how we can help with foreclosure defense can be obtained by clicking here.

Our office regularly defends its clients in court and litigation defense is one of the strategies used to challenge alleged debt obligations, and/or to win time and leverage for our clients to negotiate with their creditors.

Please call us at (631) 271-3737, or e-mail us at weiss@ny-bankruptcy.com for a free consultation to discuss litigation defense options in greater detail.

Need much here on all types of litigation and defense other than foreclosure , ie credit card, taxes, landlord tenant, student loans, medical debt, business debt, Q of personal guarantee personal injury, real estate Etc.

DEBTOR-CREDITOR LITIGATION – IN GENERAL

Legal disputes over debts and financial obligations that cannot be initially resolved or compromised are resolved in various ways: litigation, arbitration and/or mediation. Litigation which is the most adversarial method is also the most prevalent method of dispute resolution. Litigation involves a contested proceeding subject to civil procedure rules and the rules of the court where the opposing sides try to convince the fact finder (a judge or a jury) that their side should prevail based on the evidence presented, the applicable agreements between the parties (loan documents, contracts, leases and other written or oral understandings) the laws (statutory and case law) as they apply to the situation. When litigation is uncontested and the defendant defaults, and there is a default judgment ultimately entered, the litigation moves faster. When there is a contested proceeding, the litigation moves more slowly and neither side will know exactly what the outcome will be until the fact finder makes a determination. Therefore, there is pressure in a litigation to settle, when the effort, time costs and attorney fees involved can be significant. Most litigations ultimately settle, since after the posturing by each side initially in the litigation, it becomes clearer what the risks are for each side. When the debt dispute is over a relatively smaller amount of money there is more pressure to settle. When the litigation does not settle it goes through the following steps:

Legal disputes over debts and financial obligations that cannot be initially resolved or compromised are resolved in various ways: litigation, arbitration and/or mediation. Litigation which is the most adversarial method is also the most prevalent method of dispute resolution. Litigation involves a contested proceeding subject to civil procedure rules and the rules of the court where the opposing sides try to convince the fact finder (a judge or a jury) that their side should prevail based on the evidence presented, the applicable agreements between the parties (loan documents, contracts, leases and other written or oral understandings) the laws (statutory and case law) as they apply to the situation. When litigation is uncontested and the defendant defaults, and there is a default judgment ultimately entered, the litigation moves faster. When there is a contested proceeding, the litigation moves more slowly and neither side will know exactly what the outcome will be until the fact finder makes a determination. Therefore, there is pressure in a litigation to settle, when the effort, time costs and attorney fees involved can be significant. Most litigations ultimately settle, since after the posturing by each side initially in the litigation, it becomes clearer what the risks are for each side. When the debt dispute is over a relatively smaller amount of money there is more pressure to settle. When the litigation does not settle it goes through the following steps:

- Pleadings – the plaintiff must serve the defendant with a “summons and complaint” alleging the initial causes of action and the alleged damages of the defendant. Service of process which can be personal, substitute of “nail and mail” (affixing to the door) at the defendant’s residence or principal place of business. The defendant within 20-30 days after service of process needs to answer the complaint with a document called an “answer” which involves denials and defenses to the allegations. The defendant can also counterclaim or sue the plaintiff back for similar or different allegations. The effect of the counterclaims is that the plaintiff also needs to answer in a document called “reply to counterclaims”. Besides answering the complaint the defendant can alternatively make a motion to dismiss if the defendant believes that the allegations even if they were true do not constitute a cause of action.

- Conferences – Most courts try to bring both sides together to the court in some manner in order to encourage resolution and potential settlement. During the conferences the Court asks each side separately or together about pertinent aspects of the case, their positions, whether they took into account the opposing positions and whether they are ready or willing to settle. Courts recognize that voluntary settlements are more efficient and more accepted by the parties and therefore should be encouraged whenever possible.

- Discovery – Discovery is sought in a contested proceeding where information and documentation is sought from the other side in the litigation or from others who may have information/ documents that may help with needed information for the litigation. Usually discovery is in the form of: a) Document Demands (legal documents, receipts, invoices, bank statements, tax returns etc.); b) Interrogatories (questions asking for information pertaining to the issues in the case; c) Depositions (legal questioning of the other litigants or other witnesses or persons with information about the case; d) Bill of Particulars (an attempt to get more detail about the allegations). Where the two sides have a dispute about discovery it can be resolved by a Motion to Quash Discovery made by one side to protect itself or by a Motion to Compel Discovery where one side believes that other side is intentionally withholding discovery. There are grounds to object to discovery based on relevancy, the request being overly broad, the request being overly burdensome, the information being privileged information and/or the information not being within the control of the litigant served with the demand.

- Motion Practice – The next stage in the case is motion practice in cases where there are no major factual disputes and the contest between the two sides is to interpret, analyze, argue, and draw conclusions about the mostly known and mostly agreed upon facts. The usual motions are either a motion for a default judgment where the defendant does not answer or a motion for summary judgment where the defendant does answer. In a motion for summary judgment the plaintiff argues from the position that even if everything that the defendant is stating in their defense is true, the plaintiff would still prevail in their suit based on the law. In a motion for a default judgment the plaintiff alleges that the defendant was served correctly and given adequate time under the law to respond but the defendant has failed to do so and therefore the plaintiff should be allowed to prevail. There are also motions that deal with asking the Court to vacate and/or reconsider a decision: a motion to vacate an order, a motion to reargue, a motion to renew, a motion for a stay pending appeal and/or a motion for a new trial. There are many other kind of motions depending on the litigation type and the posture of the litigants.

- Trial and/or Evidentiary Hearing – Where facts are in dispute a trial and/or an evidentiary hearing is necessary for the court to be able to determine the facts. Evidentiary hearings are more limited and concentrated on a specific question of fact. For example a Traverse Hearing is focused on the issue of service of process and whether the plaintiff has obtained jurisdiction for the court over the defendant. A trial is more involved and often deals with multiple issues pertaining to a case.

- Order to Show Cause – An Order to Show Cause is an expedited and/or emergency motion that is brought to Court on shortened notice and seeks to have the Court render a quick decision on an important matter and/or a stay of imminent action pending the Court’s determination. Orders to Show Cause typically are filed to stop immediate devastating events, like a foreclosure sale, an eviction, a bank seizure, a wage garnishment and any other actions that may harm the plaintiff.

- Decision / Order – This is the decision for better or worse of the Court hearing the case (Supreme Court). Where the Court renders an order which is relatively short giving its decision (long form order) and may explain the order in either another longer version of the order (short form order) or in a decision which is more expansive.

- Appeal – A litigant can appeal an adverse decision or order that is either a final decision to the case or an interlocutory decision. An appeal needs to be taken through a notice of appeal within 30 days after the notice of entry for a decision. The notice of appeal notifies the other parties and the court that a litigant intends to file an appeal. The actual memorandum brief for the appeal is due within six months of the the notice of appeal and is a comprehensive and thorough argument as to the issues by the litigant.

DEBTOR-CREDITOR LITIGATION – DEFENSE

Litigation Defense is a concentration of our our law office because it is a tool in our overall mission of debt relief for our clients. Litigation Defense allows clients to defend against various forms of collection actions. The goal of Litigation Defense is to question and challenge the underlying presumptions of the creditor which are that they should collect on debt because it is owed. We challenge the underlying agreements for the debt, the interim invoices and other transactions, the terms of the agreement, who breached the agreement first and the methods used in collecting on the debt. The goals of litigation are usually a negotiated settlement that is favorable for our client; however sometimes a creditors mistake is an opportunity for a dismissal or other strategic advantage such as a counterclaim for consumer law violations. The strategy for a defendant is to pursue procedure over substance (ie issues of service, notice, documentary issues etc.). The other strategy is to deny all/most allegations and to force the plaintiff to prove every aspect of their case. By the defendant not conceding to anything; the plaintiff will need to have to prove every aspect of their case; the goal is time, leverage and the element of surprise with many creditors not expecting resistance /opposition to their methods. The advantage of Litigation Defense is that the creditor may not be prepared for it. The disadvantage is that the time /cost/ expenses of litigation make smaller disputes with smaller amounts at stake, untenable in terms of long term litigation.

Litigation Defense is a concentration of our our law office because it is a tool in our overall mission of debt relief for our clients. Litigation Defense allows clients to defend against various forms of collection actions. The goal of Litigation Defense is to question and challenge the underlying presumptions of the creditor which are that they should collect on debt because it is owed. We challenge the underlying agreements for the debt, the interim invoices and other transactions, the terms of the agreement, who breached the agreement first and the methods used in collecting on the debt. The goals of litigation are usually a negotiated settlement that is favorable for our client; however sometimes a creditors mistake is an opportunity for a dismissal or other strategic advantage such as a counterclaim for consumer law violations. The strategy for a defendant is to pursue procedure over substance (ie issues of service, notice, documentary issues etc.). The other strategy is to deny all/most allegations and to force the plaintiff to prove every aspect of their case. By the defendant not conceding to anything; the plaintiff will need to have to prove every aspect of their case; the goal is time, leverage and the element of surprise with many creditors not expecting resistance /opposition to their methods. The advantage of Litigation Defense is that the creditor may not be prepared for it. The disadvantage is that the time /cost/ expenses of litigation make smaller disputes with smaller amounts at stake, untenable in terms of long term litigation.

DEBTOR-CREDITOR LITIGATION – OFFENSE / PROSECUTION

Although we intuitively take to the defendants’ side because we associate that side with the smaller party, usually a consumer or small business owner or individual; in many instances we can take the plaintiff’s side very comfortably because ultimately we are still within the substantive legal areas in which we practice, which are to protect the rights of consumers and seek resolutions for small business owners and individuals who seek to affordably litigate their rights. We can initiate litigations where called upon; usually in the consumer credit situation, but in many other situations where we need to seize the initiative to resolve a dispute for our client who needs to commence litigation proceedings to resolve their situation. Often in the debt collection area, there is a gap in the creditor’s procedure where we can potentially prevail if we bring things to court. In Litigation Offense / Prosecution we are called upon to draft the summons and complaint and to plan on serving it and filing affidavits of service with the court. Afterward, unless there is negotiated settlement, we proceed to find a way to prevail in the litigation.

Although we intuitively take to the defendants’ side because we associate that side with the smaller party, usually a consumer or small business owner or individual; in many instances we can take the plaintiff’s side very comfortably because ultimately we are still within the substantive legal areas in which we practice, which are to protect the rights of consumers and seek resolutions for small business owners and individuals who seek to affordably litigate their rights. We can initiate litigations where called upon; usually in the consumer credit situation, but in many other situations where we need to seize the initiative to resolve a dispute for our client who needs to commence litigation proceedings to resolve their situation. Often in the debt collection area, there is a gap in the creditor’s procedure where we can potentially prevail if we bring things to court. In Litigation Offense / Prosecution we are called upon to draft the summons and complaint and to plan on serving it and filing affidavits of service with the court. Afterward, unless there is negotiated settlement, we proceed to find a way to prevail in the litigation.

KINDS OF DEBTOR-CREDITOR LITIGATION –

Business Debt Litigation

Most businesses constantly have regular money obligations and have liability to others and in turn are owed money by their own customers. Most businesses also need credit in the forms of loans. The loans can be both secured loans where is collateral given to the creditor in case of default, or unsecured loans where there is no collateral. The loans can also be guaranteed or not guaranteed. These money obligations and loans are frequently in litigation when there are interruptions with the flow of business income, the businesses is struggling and/or the business is going through financial hardship. We can defend both the business and the individual in a litigation initiated to establish the businesses liability; we can also embark on litigation offense to collect on monies or debt owed to the business Also businesses have contracts, leases, arrangements with independent and sub contractors and employees that can become problematic and end up in litigation. Finally businesses can have buy/sell agreements for the entire business or parts of the business where the is litigation between the new and old owners. There are many possible contested issues in a business litigation. Among to possible issues are: contesting the notice/declaration of the default, contesting the alleged breach or who breached first, contesting a personal guarantee, contesting a secured interest, contesting the amount of liability and contesting if the defendant has a right to cure. What is unique about business litigation is that service of process, noticing issues and other procedural safeguards in place with individual are diminished when the litigation is considered to be a commercial litigation and the defendant is a corporation. Service of process can be on the secretary of state for a business, the usury defense and predatory lending defense and other defenses that protect consumers are not going to give the same protections as to an individual. However, when both the business corporation and its individual owner are sued together, the owner, as an individual, may have some of these consumer defenses apply. We are often called upon to protect our client’s interests in a business litigation.

Most businesses constantly have regular money obligations and have liability to others and in turn are owed money by their own customers. Most businesses also need credit in the forms of loans. The loans can be both secured loans where is collateral given to the creditor in case of default, or unsecured loans where there is no collateral. The loans can also be guaranteed or not guaranteed. These money obligations and loans are frequently in litigation when there are interruptions with the flow of business income, the businesses is struggling and/or the business is going through financial hardship. We can defend both the business and the individual in a litigation initiated to establish the businesses liability; we can also embark on litigation offense to collect on monies or debt owed to the business Also businesses have contracts, leases, arrangements with independent and sub contractors and employees that can become problematic and end up in litigation. Finally businesses can have buy/sell agreements for the entire business or parts of the business where the is litigation between the new and old owners. There are many possible contested issues in a business litigation. Among to possible issues are: contesting the notice/declaration of the default, contesting the alleged breach or who breached first, contesting a personal guarantee, contesting a secured interest, contesting the amount of liability and contesting if the defendant has a right to cure. What is unique about business litigation is that service of process, noticing issues and other procedural safeguards in place with individual are diminished when the litigation is considered to be a commercial litigation and the defendant is a corporation. Service of process can be on the secretary of state for a business, the usury defense and predatory lending defense and other defenses that protect consumers are not going to give the same protections as to an individual. However, when both the business corporation and its individual owner are sued together, the owner, as an individual, may have some of these consumer defenses apply. We are often called upon to protect our client’s interests in a business litigation.

Student Loan Debt Litigation

Student Loans are generally divided into two groups: (1) Student loan programs backed by the government (usually it’s the federal government involved with these loan programs)(“Government Loans”); and (2) Student loans obtained from private sources. (“Private Loans”). Most persons borrowing for their education first borrow from the Government Loans but when these max out they look for Private Loans for the rest of the loans. The treatment for both kinds of Student Loan debts is very different and therefore there are different strategies for both. The Government Loans are more willing to allow borrowers to enter into repayment plans including income based repayment plans, while the Private Loans are not generally as lenient. However the NY State statute of limitations of six (6) years applies to the Private Loans but not to the Government Loans. So the Government Loans are easier to deal with by negotiated payment plan programs while the Private Loans are harder to negotiate and usually need to be refinanced for better terms or when that is not possible defended in a litigation. At issue with Private Loans are often guarantees by the borrower’s parents/relatives; were they aware of them and were they conspicuous, were notarized and actually signed with an original signature? Does the lender imply in its literature that it works with borrowers when they experience hardship? Are the reasons for the non-payment sympathetic and potentially shielded by any kinds of laws (ie health related) notice related? Were the amounts of the liability/ and the terms clear? Was the lender trying to help resolve through negotiations? Where the person owing the debt does not have the ability to pay they could allege that lender unfair with not considering them for payment relief plans when the defendant demonstrated a clear need for reorganized/deferred terms and the lender seams to allow lacking in any set standardized criteria for considering payment plans.

Student Loans are generally divided into two groups: (1) Student loan programs backed by the government (usually it’s the federal government involved with these loan programs)(“Government Loans”); and (2) Student loans obtained from private sources. (“Private Loans”). Most persons borrowing for their education first borrow from the Government Loans but when these max out they look for Private Loans for the rest of the loans. The treatment for both kinds of Student Loan debts is very different and therefore there are different strategies for both. The Government Loans are more willing to allow borrowers to enter into repayment plans including income based repayment plans, while the Private Loans are not generally as lenient. However the NY State statute of limitations of six (6) years applies to the Private Loans but not to the Government Loans. So the Government Loans are easier to deal with by negotiated payment plan programs while the Private Loans are harder to negotiate and usually need to be refinanced for better terms or when that is not possible defended in a litigation. At issue with Private Loans are often guarantees by the borrower’s parents/relatives; were they aware of them and were they conspicuous, were notarized and actually signed with an original signature? Does the lender imply in its literature that it works with borrowers when they experience hardship? Are the reasons for the non-payment sympathetic and potentially shielded by any kinds of laws (ie health related) notice related? Were the amounts of the liability/ and the terms clear? Was the lender trying to help resolve through negotiations? Where the person owing the debt does not have the ability to pay they could allege that lender unfair with not considering them for payment relief plans when the defendant demonstrated a clear need for reorganized/deferred terms and the lender seams to allow lacking in any set standardized criteria for considering payment plans.

Credit Card Debt Litigation

Credit card debt is the most prevalent debt that consumer debtors default on and for which they seek Chapter 7 bankruptcy relief. However there are many instances where Chapter 7 is either not possible, not safe and/or otherwise not desired by the person owing the debt. Usually negotiation of the debt is the next alternative to bankruptcy, however negotiations don’t always succeed in a vacuum and it often helps to contest the debt in order to obtain time and leverage to negotiate. Sometimes there are real issues that cause the debtor to believe an alleged debt is in error, not owed at all and/or overly stated and miscalculated. Credit card litigation is usually based on the procedural and technical deficiencies which undermine the essence of the collection effort. The main goal of the defendant where it lacks a substantive issue is to press the lender to prove that they have the power to collect on the debt. Often there are significant technical issues like a violation of the statute of limitations on debt where the collection action is filed more than six (6) years after the default and/or a lack of jurisdiction due to the failure to properly serve the defendant by good personal, substitute or “nail and service” at their domicile. Other technical issues are challenging the alleged signed paper work, signed receipts, and demanding to see the original signed contract with the credit card. More substantive issues are potential fraud and or identity theft where there are charges that the defendant does not recognize and/or that the debt was charged by an entity that the defendant does not recognize. This is especially true where charges where on line or on a phone line. Other approaches are to contest the interest/penalty calculation. One strategy is not just to defend the action but also to counterclaim, if applicable based inter alia on the creditors potential violations of federal and New York State debt collection statues, like the Fair Debt Collection Practices Act, when they have reason to believe that their collection action may be found wanting of cause and abusive. At the end this strategy works well for higher amounts of credit card debt that is being litigated, since litigation is time consuming and has its own costs. However, for the lower level credit debt that is usually being litigated by us, the litigation should be coupled with credit card debt negotiation, to keep costs manageable. No matter what the debt load for credit cards, most creditors are not expecting litigation defense for credit cards, since most defendants do not realize that the defense option is real. Therefore credit card debt litigation can be effective with the appropriate facts when dealing with appropriate circumstances.

Credit card debt is the most prevalent debt that consumer debtors default on and for which they seek Chapter 7 bankruptcy relief. However there are many instances where Chapter 7 is either not possible, not safe and/or otherwise not desired by the person owing the debt. Usually negotiation of the debt is the next alternative to bankruptcy, however negotiations don’t always succeed in a vacuum and it often helps to contest the debt in order to obtain time and leverage to negotiate. Sometimes there are real issues that cause the debtor to believe an alleged debt is in error, not owed at all and/or overly stated and miscalculated. Credit card litigation is usually based on the procedural and technical deficiencies which undermine the essence of the collection effort. The main goal of the defendant where it lacks a substantive issue is to press the lender to prove that they have the power to collect on the debt. Often there are significant technical issues like a violation of the statute of limitations on debt where the collection action is filed more than six (6) years after the default and/or a lack of jurisdiction due to the failure to properly serve the defendant by good personal, substitute or “nail and service” at their domicile. Other technical issues are challenging the alleged signed paper work, signed receipts, and demanding to see the original signed contract with the credit card. More substantive issues are potential fraud and or identity theft where there are charges that the defendant does not recognize and/or that the debt was charged by an entity that the defendant does not recognize. This is especially true where charges where on line or on a phone line. Other approaches are to contest the interest/penalty calculation. One strategy is not just to defend the action but also to counterclaim, if applicable based inter alia on the creditors potential violations of federal and New York State debt collection statues, like the Fair Debt Collection Practices Act, when they have reason to believe that their collection action may be found wanting of cause and abusive. At the end this strategy works well for higher amounts of credit card debt that is being litigated, since litigation is time consuming and has its own costs. However, for the lower level credit debt that is usually being litigated by us, the litigation should be coupled with credit card debt negotiation, to keep costs manageable. No matter what the debt load for credit cards, most creditors are not expecting litigation defense for credit cards, since most defendants do not realize that the defense option is real. Therefore credit card debt litigation can be effective with the appropriate facts when dealing with appropriate circumstances.

Tax Debt Litigation

Tax debt litigation is usually not the preferred first approach to income tax debt where there is usually an effort by the debtor-tax payor to seek an negotiated solution and/or payment plan with the taxing authorities, the Internal Revenue Service (“IRS”) or the New York Department of Taxation and Finance (“NYS”). However, where the IRS and/or NYS are inflexible and there are potentially real unanswered questions about the alleged liability and/or the amount of the alleged liability tax debt, litigation can be an alternative that causes the the taxing authorities to look again at their methods in the case at hand and see that they may want to compromise, especially when the tax case is laid out nicely by attorneys for the tax payor. The first question with tax debt is whether the tax years in question have been filed. If not, which is often the case, the tax transcripts need to be obtained and these then need to be the basis for the filing of the tax returns, which are always better filed, than still being un-filed. Once the tax returns are prepared for the missing tax years and then immediately submitted to the taxing authorities, the situation will usually start to simplify where the taxing authorities and/or the Courts go by the amounts asserted by the defendant in their recently filed returns which are relatively low. However, where the taxing authorities do not accept these numbers or where there are other problems, litigation may be necessary which can take place in several courts:

Tax debt litigation is usually not the preferred first approach to income tax debt where there is usually an effort by the debtor-tax payor to seek an negotiated solution and/or payment plan with the taxing authorities, the Internal Revenue Service (“IRS”) or the New York Department of Taxation and Finance (“NYS”). However, where the IRS and/or NYS are inflexible and there are potentially real unanswered questions about the alleged liability and/or the amount of the alleged liability tax debt, litigation can be an alternative that causes the the taxing authorities to look again at their methods in the case at hand and see that they may want to compromise, especially when the tax case is laid out nicely by attorneys for the tax payor. The first question with tax debt is whether the tax years in question have been filed. If not, which is often the case, the tax transcripts need to be obtained and these then need to be the basis for the filing of the tax returns, which are always better filed, than still being un-filed. Once the tax returns are prepared for the missing tax years and then immediately submitted to the taxing authorities, the situation will usually start to simplify where the taxing authorities and/or the Courts go by the amounts asserted by the defendant in their recently filed returns which are relatively low. However, where the taxing authorities do not accept these numbers or where there are other problems, litigation may be necessary which can take place in several courts:

1) The U.S. Bankruptcy Court -Like the Tax Court below the taxpayer with a dispute can delay payment without penalty while their legitimate case is being litigated. The U.S. Bankruptcy Court has broad discretion over issues like liability, amount of the liability, techniques of debt collection by the IRS, whether certain defenses like innocent spouse and/or innocent officer should apply. Generally clients owing tax debt owe other kinds of debt as well and the Bankruptcy Court allows resolutions for taxes in every tax case, whether Chapter 7, 11 and/or 13. Bankruptcy Court is considered to be a debtor friendly jurisdiction because it is not automatically partial to the Government’s case?

2) The U.S. Tax Court – Like the U.S. Bankruptcy Court, the U.S. Tax Court is another jurisdiction where the tax payer has the advantage of delaying payment until there is a court resolution. In all other forums the taxpayer needs to first pay and litigate and only if their win can the taxpayer ask for a refund. The U.S. Tax Court, having 19 judges, is located in Washington D.C. as well as having a traveling presence depending on which cities some of judges decide to travel to. The U.S. Tax Court unlike some of the other courts does not have general jurisdiction, but specialized jurisdiction to review and hear the tax case only. The Court has broad discretion to review many tax related issues including the existence and amount of the alleged IRS liability, the collection methods used, the noticing requirements and whether they were met, the reasonableness of IRS in refusing an offer in compromise of other proposed resolution.

3) The U.S. District Court – This is a court of general jurisdiction for the U.S. Court system and takes on the initial stage of any controversy, although for the Bankruptcy Courts it has become a court of appellate review where a decision in the Bankruptcy Court is appealed. If a tax debt is not unbearably high and can first be paid or if it was paid already, the U.S. District Court has it’s advantages in that it is a more general jurisdiction federal court and therefore may be more sympathetic to a taxpayers situation if the taxpayer is mostly wrong technically; or

4) The U.S. Court of Claims – This is a court usually for large international companies and does not usually apply to our clients.

Because in collecting on debt the taxing authorities have become very powerful and potentially akin to a prosecutor, judge and jury all rolled into one, there need to be and there are some safeguards. That is why important issues need to go to a Court when there is a dispute with the taxing authorities. There are many different issues that can and sometime should go before the Courts to get a third party’s decision involved. Issues that the courts above could decide include:

a) Liability for the Tax Debt ?- The first question is whether the tax debt in the form and in the amount of the tax debt sought by IRS should be owed after the client has been diligent with tax returns, transcripts and other proof of income which according to the taxpayer show that the debt should be cancelled and/or substantially reduced?

b) Amount of Tax Debt? – The next question is whether all the sub-components are of the alleged tax debt are owed in the amounts asserted?

c) Defense to the Tax Debt Obligation? – A follow question is whether possible defenses can apply: Innocent spouse? Innocent officer? Alleged “employees” are really independent contractors? The expenses incurred were business and not personal expenses? And/or other potential defenses?

d) Deductions Apply?– Did certain deductions apply to reduce the tax debt? Certain credits, reductions and/or adjustments that would result in lesser taxes due?

e) Any Setoff Apply? (Due to Past Losses Which are Possible Credits Towards Present Gains) – Despite all of the above should the taxpayer get past tax debt setoffs to bring down the debt presently owed?

f) Whether the Taxing Authority has Unfairly DenIed an Offer in Compromise and/or Other Payment Plan? Does the taxpayer’s situation compel an offer in compromise being given? Does the tax payer deserve temporary “uncollectible” status? Can the taxpayer pay under a payment plan? Does the taxpayer qualify for a “partial payment installment payment plan”?

g) Whether the Taxing Authority Should Exercise Discretionary Leniency– Whether certain facts created a sympathetic situation arguing for discretionary leniency and forgiveness of all/part of the debt? IE, theft, fire, accounting problems, disaster recovery, illness, Covid-19 losses etc.

Landlord-Tenant Litigation

The goal in Landlord-Tenant Litigation is to show that the other party breached and/or that the other party breached first. Our office represents both tenants and smaller landlords. Both tenants and smaller landlords are vulnerable economically and small changes in their finances may affect their ability to meet their obligations. For that reason litigation is important. For a small landlord litigation may be the only way to end a financially draining problem. For a tenant litigation may be the only way to hang on temporarily and survive as they recover from an economic setback like job loss, marital difficulties or other interruptions to their finances.

The goal in Landlord-Tenant Litigation is to show that the other party breached and/or that the other party breached first. Our office represents both tenants and smaller landlords. Both tenants and smaller landlords are vulnerable economically and small changes in their finances may affect their ability to meet their obligations. For that reason litigation is important. For a small landlord litigation may be the only way to end a financially draining problem. For a tenant litigation may be the only way to hang on temporarily and survive as they recover from an economic setback like job loss, marital difficulties or other interruptions to their finances.

As TENANT, if there are non-rent issues with the landlord, the the best way to overcome such non-rent issues, is to isolate problems of landlord and stay current and to start a suit against the landlord. That is because the lease is usually drafted by the landlord who specifically disallows deduction of rent as a self-help measure and deems it to be a breach of the lease and a default (despite any justification). The tenant if they are prosecuting the lawsuit want to show violations of the lease and of the law and to cast themselves as the aggrieved party. If successful the tenant may be owed money, some months of credit and/or “free’ rent, agreements by the landlord to fix certain problems with the building/rental apartment. On the other hand if the the tenant is defending which is much more often, the tenant is usually also behind on payment of rent and needs to try to zealously contest the landlord’s allegations and procedure in commencing the litigation with a RESPONSE to the landlord’s PETITION, which is like an answer to a complaint. The tenant needs to contest the basis of the alleged default, and try to show that it has not violated the lease. When possible the tenant can dispute receipt/service of the notice to cure, service of petition, and other procedure. The tenant may allege an understanding with the landlord that the landlord changed his mind on, deficient services of landlord that are supposed to be provided under the lease or by law, violations by landlord, failure by the landlord to provide a safety/security, issues with the providing and/or payment for utilities, needed repairs, dysfunctional systems and/or ongoing nuisances that interfere with the use and habitability.

For COOP RESIDENTS with proprietary leases the landlord tenant proceeding is a much more pitched battle because the greater issues at stake, the continued right of the coop resident to live in their unit. Disputes with coop boards are common since boards and their approaches/attitudes change and this leads to a potential lack of predictability as to enforcement of rules, imposition of policies and/or the interpretation of those rules/policies. If there is a dispute, often the board charges the resident with the legal fee thereby exacerbating tensions and escalating the dispute.

AS LANDLORD – It is important to document problems and to give tenants notices which serve two purposes: a) notices document that the event took place; and b) notices show that the tenant was given warning and an opportunity to correct the situation; c) notices show fairness, a lack of arbitrariness, abruptness, lack of bias or other malevolent motives. Besides rent arrears other matters may be cause for warnings and eventual lease termination, ie smoking, pets, drugs, loud music. Besides the informal notices discussed above, there are pre-eviction notices that need to be served 30, 60, or 90 days prior to start of the eviction depending on the amount of time the tenant was at the property. (See the Landlord Tenant Solutions Section of this website for more information). After giving the required notices, the Landlord can start an eviction proceeding by filing and serving all tenants in violation and by making sure that all separate rentals are served. Currently there is still an eviction moratorium in New York State that at this point expires on August 31, 2021, unless further extended by the NYS legislature. Until this moratorium is over for an eviction action to go forward, there would need to be a showing that the tenant is a danger to others and/or that the tenant creates a nuisance to others.

Foreclosure Defense Litigation

Foreclosure Defense is defending a litigation commenced by a mortgage holder to foreclosure on real estate where the mortgage loan is in default. Foreclosure defense is needed by a defendant/borrower to avoid allowing the mortgage holder to easily obtain a default judgment and gives the borrower leverage and time to potentially come up with alternate resolutions to resolve the foreclosure. Jurisdiction (service, residency), Notices (90 day notice, 90 day affidavit, default notice, acceleration notice) , default (was the d in default?), acceleration, understandings about catching up, robo-signing, lack of original paper work, standing, possession, predatory, payments not accounted, motion to extend time to answer referee report inaccurate – no notice of the report, reargument/renewal, notice of appeal, stay pending appeal, perfection of appeal, multiple appeals. OSC to vacate prior decision granted on default, OSC to stay a foreclosure sale.

Foreclosure Defense is defending a litigation commenced by a mortgage holder to foreclosure on real estate where the mortgage loan is in default. Foreclosure defense is needed by a defendant/borrower to avoid allowing the mortgage holder to easily obtain a default judgment and gives the borrower leverage and time to potentially come up with alternate resolutions to resolve the foreclosure. Jurisdiction (service, residency), Notices (90 day notice, 90 day affidavit, default notice, acceleration notice) , default (was the d in default?), acceleration, understandings about catching up, robo-signing, lack of original paper work, standing, possession, predatory, payments not accounted, motion to extend time to answer referee report inaccurate – no notice of the report, reargument/renewal, notice of appeal, stay pending appeal, perfection of appeal, multiple appeals. OSC to vacate prior decision granted on default, OSC to stay a foreclosure sale.

Medical Debt Defense Litigation

Medical Debt Litigation (need new page) – Present info on site deals mostly with Medical Debt Negotiation; Here we want to go into Medical Debt Litigation; sections should cross reference each other.

who’s medical debt? (relative signing in? insured if not covered? patient if no signiture?), if patient signed – able to give consent?no advanced knowledge, lack of services,

Credit Repair Litigation and Other Consumer Rights Litigation

Credit Repair Litigation (Need New page) – Present info on site deals mostly with Medical Debt Negotiation; Here we want to go into Medical Debt Litigation; sections should cross reference each other.

HOW WE CAN HELP WITH LITIGATION AND HOW TO GET STARTED –

Appt for consult /intake. Decide on a strategy to deal with client’s issues. If decide on a litigation path we also decide on a litigation strategy.

WHY USE OUR OFFICE FOR LITIGATION

Experienced not just in lit but also in neg, mod and BK. Combine possibility of other options as leverage in that we could eliminate the debt if we prevail. Usually able to arrive at a satisfactory resolution if decision by all to settle. But if not settled can litigate and if not happy with the decision can put in notice of appeal, OSC to reconsider: vacate order, reargue or renew. Because we have such varied and effective. tools less likely that we would have creditor not give us their best possible deals.

Experienced not just in lit but also in neg, mod and BK. Combine possibility of other options as leverage in that we could eliminate the debt if we prevail. Usually able to arrive at a satisfactory resolution if decision by all to settle. But if not settled can litigate and if not happy with the decision can put in notice of appeal, OSC to reconsider: vacate order, reargue or renew. Because we have such varied and effective. tools less likely that we would have creditor not give us their best possible deals.

Contact Us

- HOURS OF OPERATION

- Monday – Friday – 8:30 AM – 8:30 PM

- Saturday – Sunday – 10 AM – 6 PM